Summary

Benchmarking your firm’s financial and operating performance provides valuable strategic information to help answer some important questions: Where do you excel and where to you fall short compared to your competitors? Are your strategic initiatives delivering expected results over time? How is your most valuable resource — your staff team — being used? Are you carrying too much overhead? Shimmerman Penn’s Architecture, Engineering and Design (AED) speciality group understands the key industry financial metrics needed to benchmark firms’ performance.

In this first instalment of the 2017 Update of key performance indicators for AED firms we will discuss the Net Fee Multiplier. The Net Fee Multiplier is a performance metric that measures a firm’s ability to convert direct labour charged to projects into revenue dollars. This metric provides an indication of how the firm has performed during the year as it has a direct relationship to profitability.

FORMULA: Net Fee Multiplier = (Net fees) / (Labour costs)

FORMULA: Net Fee Multiplier = (Net fees) / (Labour costs)

Net fees

Net fees include total revenues less all direct project costs (excluding professional salaries) which are comprised mainly of sub-consultant costs. The firm’s accounting system can be configured to capture these costs separately.

Labour costs

There are at least 2 commonly accepted methods of calculating the labour cost component of the Net Fee Multiplier and the results can vary significantly, so be careful when comparing your firm’s results to posted industry averages or those of other firms. Some firms use “direct labour” (amounts charged directly to projects) while other firms use “total professional labour” costs.

“Direct labour” will provide an accurate measure of the actual realization and may be better suited for benchmarking the profitability of projects against one another on a micro level. “Total professional labour” takes into account the impact of utilization rates and provides a more accurate macro measure of how the firm converted its labour costs into revenues.

In Shimmerman Penn’s calculations, we use “total professional labor, excluding the related employee benefits,” to factor out anomalies due to significant differences in utilization rates. This leads to results that are more comparable over time and across different firms.

Other differences can arise from the components that are included in labour costs. Additional components of labour to consider include the following:

- Labour burden (employee benefits) — may be treated as labour or overhead costs

- Employee bonuses and overtime costs — may be included if directly related to project performance

- Pursuit costs — firms that are actively involved in P3 projects are tracking the component of labour expended on RFPs.

- Owners’ salaries should be normalized at market rates to reflect the contribution for professional services rendered and should exclude time spent managing the firm. Each firm will have its own internal benchmark.

- For firms structured as partnerships, the partners commonly do not receive salaries and a “notional” salary for contribution for professional services rendered should be included in labour costs.

There is no right or wrong way to calculate Net Fee Multiplier, what’s important is that the specific methodology be applied consistently.

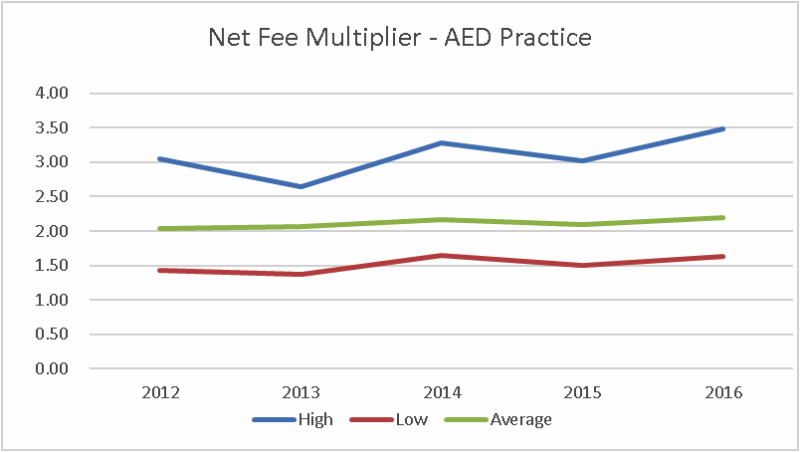

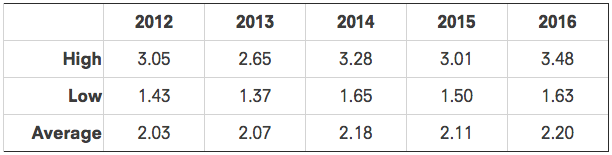

Net Fee Multiplier — 5 Year Trend And Analysis

Our methodology

Shimmerman Penn’s AED Industry Team compiled the data for the 2017 update based on annual financial results for 18 architecture and engineering client firms located within the GTA, for the fiscal years 2012 - 2016. We calculated the ratios for each firm, and then compiled the overall results using a weighted average related to each firm’s net fees.

Results and analysis

For many firms in the survey, financial performance in 2016 improved as compared to 2015.

Over the last 5 years, while the average and low Net Fee Multipliers have remained fairly consistent, some variations in the high Net Fee Multipliers indicate some firms are exploring ways in which to improve their net fee multiplier and ultimately their profitability. Firm leaders and management have learned that key factors in maintaining and improving profitability in the current environment is control over labour costs and improved project efficiency. Additionally, although it is still a very competitive market, in some sectors, both for projects and staffing, firms have been able to increase their fees over the last 2-3 years.

Benchmarking and Decision Making

How can calculating the Net Fee Multiplier be of use in your firm? We recommend that a financial dashboard be used to provide information to senior management and project managers on a regular, periodic basis. The ratio can be calculated internally on either a monthly, quarterly or annual basis. Many software platforms used by firms in this industry offer the ability to extract the data and calculate these ratios.

Benefits:

- Calculating the Net Fee Multiplier on a project-by-project basis provides useful information for evaluating efficiency and profitability of projects. This can be tracked by industry sector, project team, geographic region, etc. Compensation and performance bonus plans can be developed using these quantitative factors.

- Information regarding the firm’s historical Net Fee Multiplier can be used when developing project budgets and proposals, and in determining the optimum level of employee resources needed to staff the firm’s operations.

- Comparing to your firm’s performance over time can identify areas in which changes are occurring and assist in strategic planning and operational decision making.

- Comparing your firm against industry trends can help in strategic planning to identify areas in which changes could be made to improve profitability and efficiencies.

Benchmarking — Your Firm's Results

Our AED team can prepare a financial dashboard to compare your firm’s results to our weighted average performance indictors and assist you to understand and analyze the information.

We can assist your accounting staff to create internal reporting that captures the data from your accounting system, so that you can have these reports prepared on a regular basis.